Why I Choose UOB One Account over OCBC 360 Account! (Updates For 2021)

Today, I will be also showing you why choosing UOB One Account is the way to go for 2021!!

With so many different savings accounts that market themselves as having the ‘highest interest guaranteed!’ It is no wonder we are spoiled for choices.

Not to worry because today I will be sharing my analysis of OCBC 360 account and UOB One account.

This article will provide how each account works and how interest is calculated as well as relatable scenarios to better understand and help us make these difficult choices.

OCBC 360 Account

Fees and eligibility of the OCBC 360 Account:

To be eligible to open the account, you will have to be 18 years of age.

- 18 years old and above

- An initial deposit of $1,000

- No monthly account fees charged

- If your average daily balance falls below S$3,000, a Fall-below fee of S$2 (Waived for the first year) will be charged.

Revision of Interest Rates for OCBC 360 from 1 October 2020

From 1 October 2020 onwards, OCBC has remove the Spend and Step-up Category. Wealth Category on the other hand is split into two, insure and invest.

How does the OCBC 360 account work?

Due to changes from 2nd May 2020, you just must credit at least $1,800 of your salary.

From 1 October 2020, across the board for all category requirements, the salary tiers that will enjoy interest increased from two tiers to three tiers. Interest rates on the other hand fell.

From 1 October 2020:

- First S$25,000

- Next S$25,000

- Next S$25,000

The upcoming update is going to be in Feb 2021 and the revised version is as shown in the screen shot above.

Best credit card to pair with OCBC 360 Account

There are two credit cards to achieve the $500 spending which are OCBC titanium rewards and 90°N, however, in my opinion, they are not very favourable to most individuals.

90°N is great for travel and Titanium Rewards is good for electronics and clothing, but unless you’re regularly traveling, buying electronics, or shopping for clothes with a minimum spend of $500 per month, none of these are everyday categories.

These are cards that shine when you have large, one-off transactions to be made, not regular everyday spending.

On the other hand, the best or closes option is the OCBC 365 credit card but it requires a minimum spend of $800 which to me is also not worth it.

Check out their OCBC 360 Interest calculator !

UOB One Account

Fees and eligibility of the UOB One Account:

To be eligible to open the account, you will have to be 18 years of age.

- An initial deposit of $1,000

- Fall below fee of S$5/month (below S$1,000 balance)

- S$30 for the closing of account within 6 months of opening

- Salary Credit of $2,000

UOB One Account Revised Interest Rates from 1 Nov 2020

How does the UOB One account work?

According to their website, UOB One account offers “up to 2.50% p.a.” interest. But Looking at the breakdown above, interest is calculated based on the account balance. Therefore, the only way to get 2.50% p.a. is to have more than $60,001.

As you can see above if you are just spending $500 on your UOB One card you will receive 0.25% p.a. up till $75,000.

However, when you spend $500 on your UOB One card plus credit your salary or perform 5 Giro transactions, the interest rate is higher and goes according to your account balance.

According to my opinion, I do not think many individuals will be keeping that much spare cash in their bank and would rather invest or planning to use it to make a big purchase.

Looking at the table above, you can see clearly see that earning interest up to 2.50%p.a. is an inflated number!!

By taking $900 divided by $75,000 will give you only 1.00%!!!

Take a close look at their terms and condition below!!

1Maximum effective interest rate (EIR) on the One Account is 0.25% p.a. for deposits of S$75,000, provided customers meet the criterion of S$500 Card Spend in each calendar month. Maximum effective interest rate (EIR) on the One Account is 1.00% p.a. for deposits of S$75,000, provided customers meet both criteria of S$500 Card Spend AND 3 GIRO debit transactions in each calendar month.

Promotion now you can receive more than 2.50%!

UOB Salary Credit Campaign (4 January to 28 February 2021)

For a limited period only, you could earn up to 2.75% p.a.7 on your savings when you credit a salary of at least S$2,000 into your UOB One Account.

Terms and condition applies and for the purpose of this promotion:

Best Credit Card to pair with UOB One Account

As everyone flock to online shopping over the lockdown period to satisfy their shopaholic self, the great news here for you is that you can get up to 10% rebate for online shopping!

If you are a crazy fan of Shopee like me, then you will love how this card gives an additional 5% rebate on Shopee Singapore!

In addition you can receive up to 6% rebate on power utilities bills as well as up to 5% of rebate on all retail spend! Yes you’re right, it's ALL retail spend!

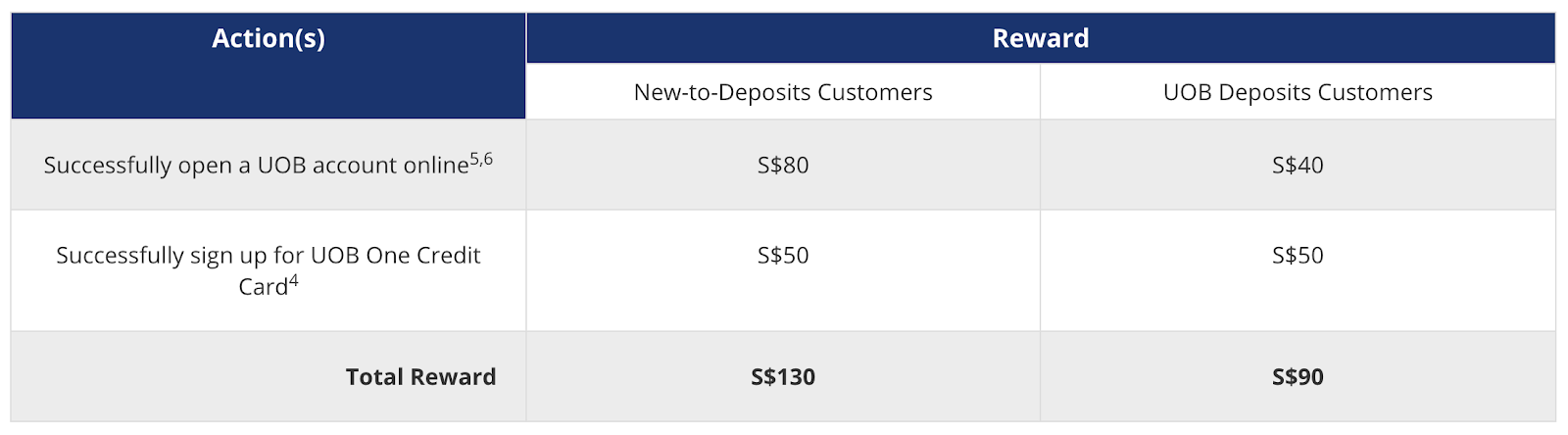

They are currently having a promotion for this as well! You get to walk away with up to $130 if you satisfy the following criteria!

Assuming I spend $100 on shopee, $150 on grab, $180 on singapore power, $120 on petrol, $100 on dining and 200 on recurring bills, my total spending for the month is $850, my quarterly rebate goes up to 50 bucks and my total cash rebate for the year is about $372! Think about taking a short trip to Bangkok… Though we can't really travel now but this money saved can be used for our future travelling still!

Check out their calculator!

Scenarios and which account!

Scenario 1: fresh Graduate with a salary of $2,500

With the changes of interest rate by OCBC, it might be better to switch to UOB One!!!

Let’s start with OCBC 360 Account

If you are a fresh graduate with a salary of $2,500, after CPF contribution your take-home pay will be $2,000 with an account balance of $15,000.

Assume you credit your salary and save at least $500 from the previous month (Salary Credit + Transaction in 1 category).

Your total interest earned is 0.3%(salary) + 0.1%(save) + 0.05%(base Interest) = 0.45%.

Compare it with UOB One account

By spending $500 on your UOB one card plus crediting your salary or making 5 giro transactions, your total interest will be 0.5%

Obvious choice UOB One account will be a winner!!

Word Of Caution!!!

In my opinion, it might not be advisable to change your account due to the interest rates as UOB might cut their interest rate as well!!!

Scenario 2: 30-year-old male with a salary of $5,000 plus account balance of $60,000

Let’s start with OCBC 360 account

If your salary is $5,000, after CPF contribution your take-home pay will be $4,000.

Assume you credit your salary and save at least $500 from the previous month (Salary Credit + Transaction in 1 category). Assuming you do not invest and buy OCBC insurance.

Because your account balance is $60,000. You earn the interest of the first tier of $25,000. Therefore, your interest amount will be $25,000 X (0.3%+0.1%) = $100

The next $25,000 will earn the interest of the next tier. Interest amount will be $25,000 X (0.6% + 0.2%) = $200

For the final $10,000 , the interest amount will be $10,000 X (1.2% + 0.4%) = $160

Your total interest rate will be ($100+$200+$160)/$60,000 = 0.767%

Compare it with UOB One account

By having $60,000 in your account balance, your total interest rate is $375/$60,000 = 0.625% if you spend $500 on your UOB one card plus crediting your salary or making 5 giro transactions.

OCBC 360 Account seems to be leading. It will be a more of a winner if you invest and buy OCBC's insurance!!

Conclusion and my personal choice

After a detailed analysis and reading through their terms and conditions. It will be impossible for me to earn the 2.50% that UOB One account offers!!!

Moral of this article is always read the terms and conditions and really understand what you are applying!!! As the saying goes “Knowledge is the new rich, arm yourselves with it.”

For fresh graduate starting like me, OCBC 360 account may seem less favourable as crediting just my salary & saving a minimum of $500 gives me ONLY 0.45% which is lower than the 0.5% that UOB One account offers.

But If my account balance goes up, OCBC 360 may be the better option!!

As I look into educating myself more on insurance and invest, I would also consider OCBC 360 as the accumulation of salary, save, invest, insure and grow gives much a way more favourable interest rate!

In addition, I get great convenience with all of my finance related documents under one account!

That said, as for now I am favouring UOB with my low income. On top of that, the on going campaign also gives me an additional perk of 0.25%! Hence, even if my account balance is only $15000, I can still earn up to 0.75% interest! Along side the promotions of earning up to $130!

Also recommending you to our youtube community! Check this sharing on the future digital bank!

Last updated on January 5th, 2021 at 04:41 pm

For scenario 2, the next tier interest rate for OCBC does not apply to the entire balance, show the EIR instead.

Hi A! ok noted. will update. Thanks =)

Hi A, thanks for the heads up! Just updated the info. Welcome to our blog! =)